Oil Slumps on COVID Fears, Oversupply, U.S. Elections

Oil was down on Wednesday morning in Asia, continuing major overnight

losses. Oversupply fears were the main driver of the fall, with U.S.

refineries beginning to shed labor.

Brent oil futures slid 1.13% to $41.09 by 11:29 AM ET (3:29 AM GMT) and WTI futures were down 0.94% to $38.92.

Heavy

falls in the previous trading session continued to drag on the Asian

markets in morning trade; WTI futures fell back below the $40 mark, with

both benchmarks losing more than 3%. The major drivers were poor

economic forecasts for future consumption amid the COVID-19 pandemic and

continued oversupply issues.

Data from the American Petroleum

Institute (API) on Tuesday showed a draw of 831,000 barrels, as against

an expected build of 1.4 million barrels, for the week ending Sept. 25,

and following the previous week’s build of 691,000 barrels. However,

this was insufficient to hold back the fall in prices.

Heads of

major energy trading companies were downbeat about future oil prices,

with low expectations of future demand and little movement in price

expected for at least months, and possibly years. “It is important to

keep in mind that moves to the downside have the potential to be

supersized,” given the COVID-19 pandemic’s continued spread and ongoing

global oversupply issues, Bob Yawger, director of energy futures at

Mizuho, told Reuters.

In signs of a protracted oversupply

problem, U.S. refineries are beginning to lay off workers, with Marathon

Petroleum Corp (NYSE:MPC), the U.S.’ largest refiner, looking to

widespread job cuts to help maintain their bottom line. Marathon

officials are “communicating with our employees about measures we

announced earlier this year to strengthen Marathon Petroleum for

short-term and long-term success,” a spokeswoman said in a statement,

according to Reuters.

Refineries globally are feeling the

pressure of a hugely depressed global air travel industry, with many

refineries attempting to blend their excess jet fuel into other products

and some installations looking likely to face shutdown.

Data

from the American Petroleum Institute (API) on Tuesday showed a draw of

831,000 barrels, as against an expected build of 1.4 million barrels,

for the week ending Sept. 25, and following the previous week’s build of

691,000 barrels. However, this was insufficient to hold back the fall

in prices.

The uncertainty over U.S. presidential elections is

also cause for concern, with President Donald Trump refusing to

guarantee a peaceful transition of power should he be ousted. The first

presidential election debate was earlier this morning and was highly

combative.

The global death toll from the COVID-19 pandemic

passed 1 million earlier in the week, and case numbers continue to rise,

further threatening global economic recovery.

Investors now await crude oil supply data from the U.S. Energy Information Administration (EIA), due later in the day.

Source : investing.com

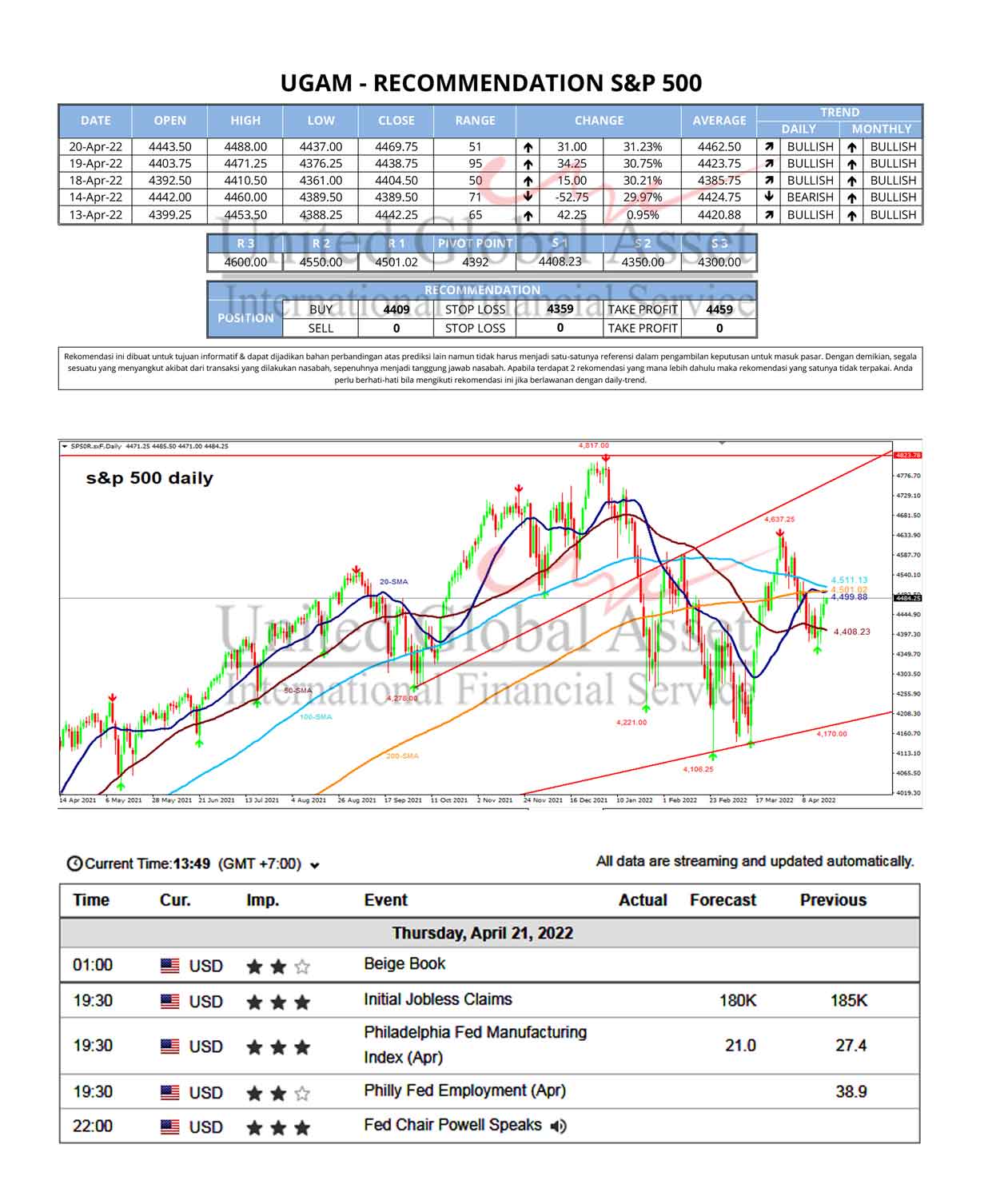

Market Recomendation

Fundamental News - S&P500

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

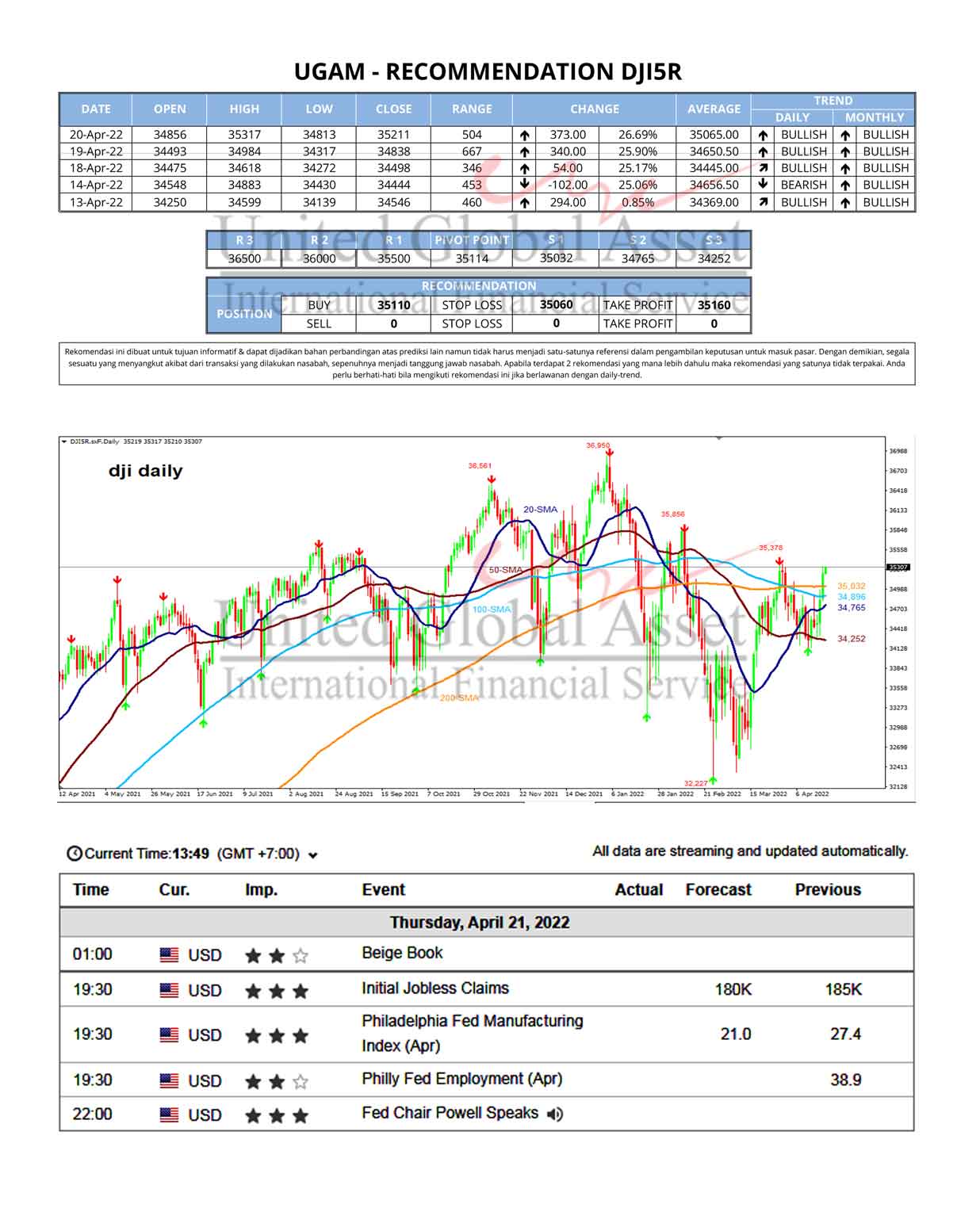

Fundamental News - DJI5R

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

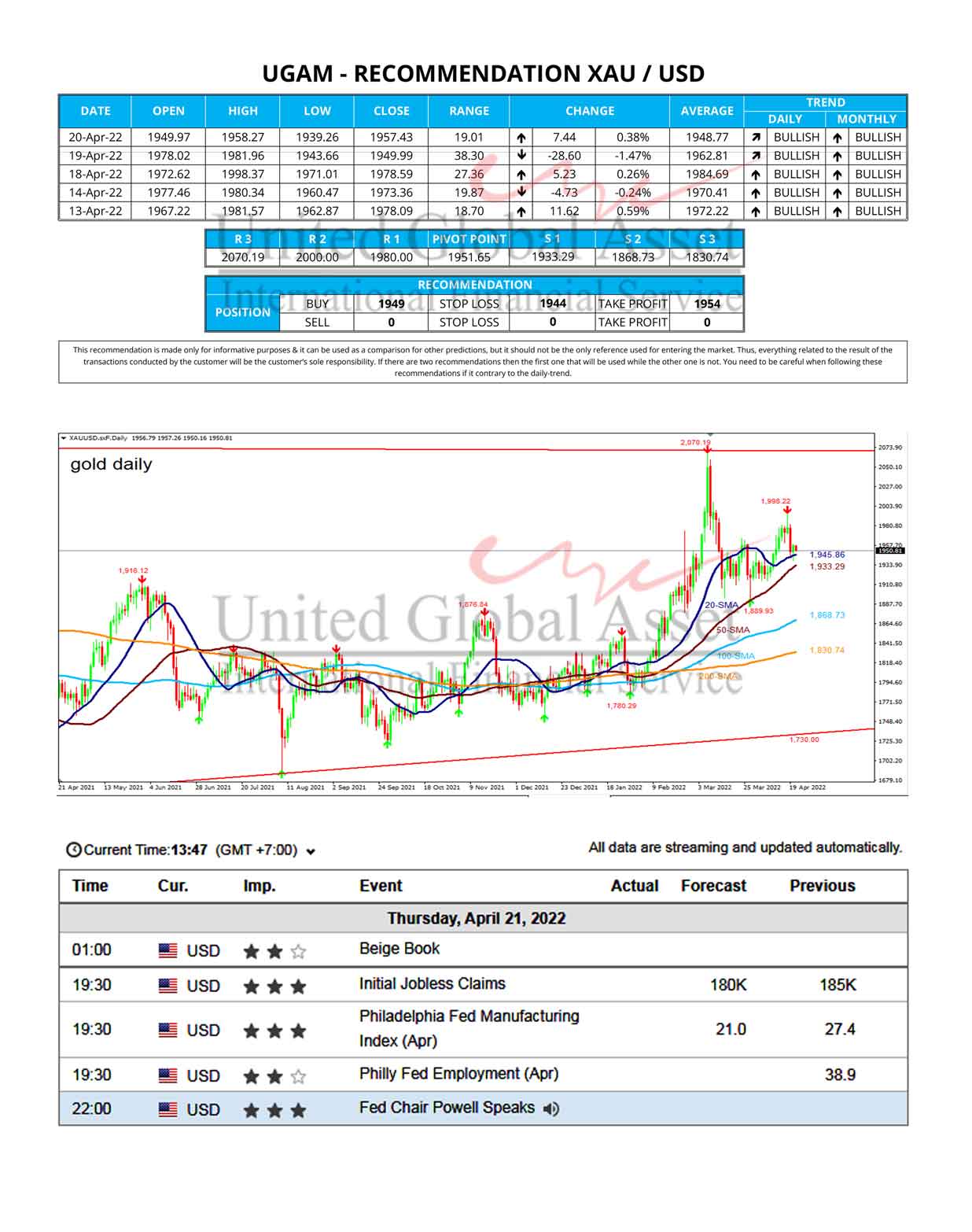

Fundamental News - XAUUSD

Gold Price is in a narrow consolidative range so far this Thursday having stalled its rebound just shy of the key $1960 level.Gold Price could see further downside risks in...