McDonalds Has More Upside Potential, According To Goldman Sachs

The fast-food giant continues to revamp both stores and the menu, and it is a solid pick for more conservative accounts. McDonald’s Corp. (NYSE: MCD) is the world’s leading global food-service retailer with over 39,000 locations serving approximately 69 million customers in over 100 countries each day. More than 80% of McDonald’s restaurants worldwide are owned and operated by independent local businesspersons.

The company has built a product pipeline, including a new chicken sandwich, a McPlant line and follow-on celebrity promos. Goldman Sachs feels the key driver of the McDonald’s story will shift to a technology scale that competitors will struggle to replicate. This tech evolution is supporting a wave of consolidation, while it creates pressure on small and mid-tier players.

The analysts said this about the fast-food giant:

We believe that McDonalds will benefit broadly from economic re-openings in 2021, and the company’s investments in technology, a renewed marketing strategy, loyalty, and menu innovation will drive share gains in the industry. We model fiscal year 2021 and 2022 same-store-sales of 16.1%/4.2% (versus Consensus 13.6%/4.1%) and unit growth slightly ahead of Consensus, which drives our fiscal year 2021 and 2022 EBITDA estimates +3.0%/+3.5% versus consensus estimates.

McDonald’s stock investors receive a 2.42% dividend. Goldman Sachs has a $237 price target, while the consensus target is higher at $241.82. The shares were last seen on Wednesday at $213.63.

Market Recomendation

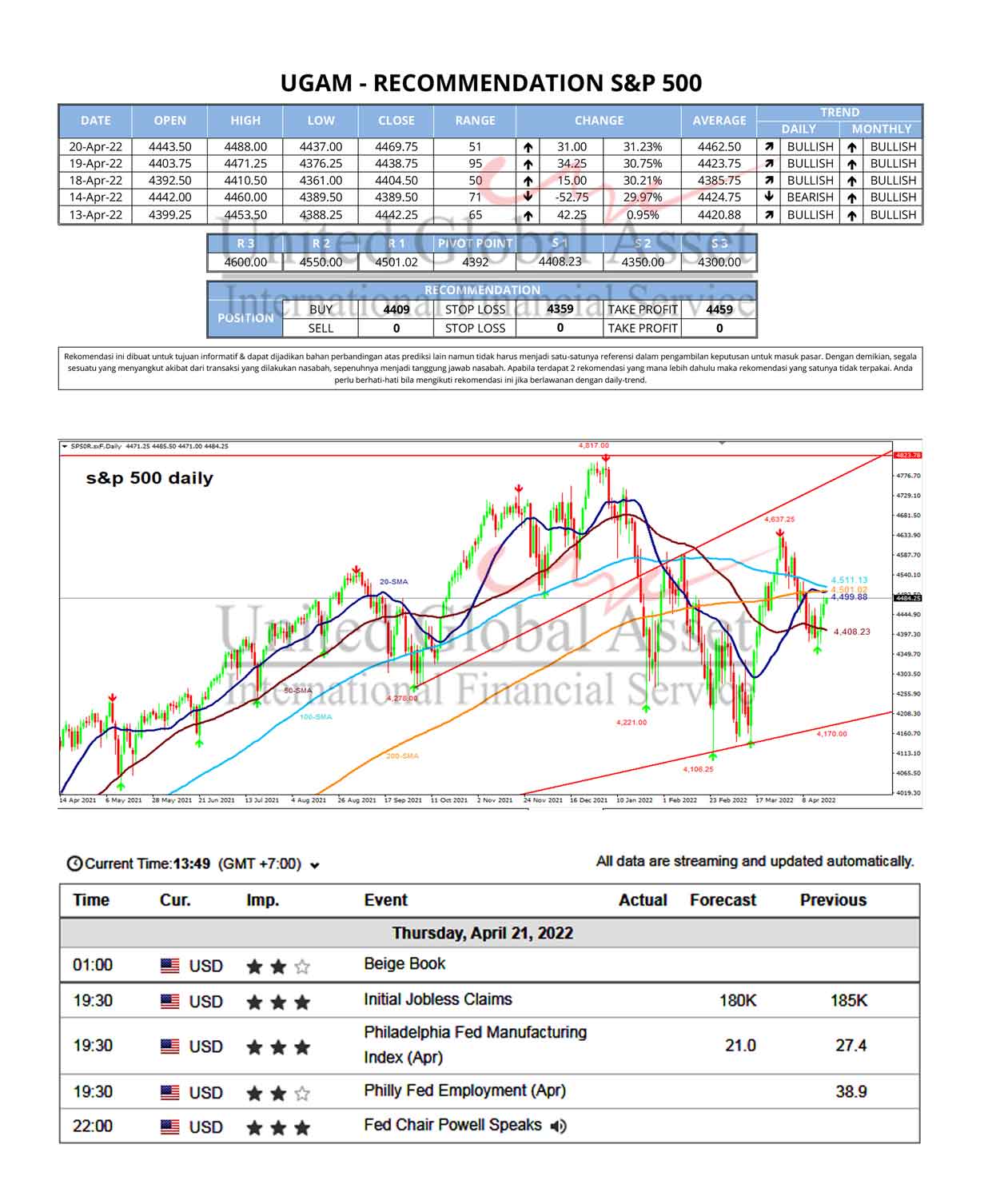

Fundamental News - S&P500

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

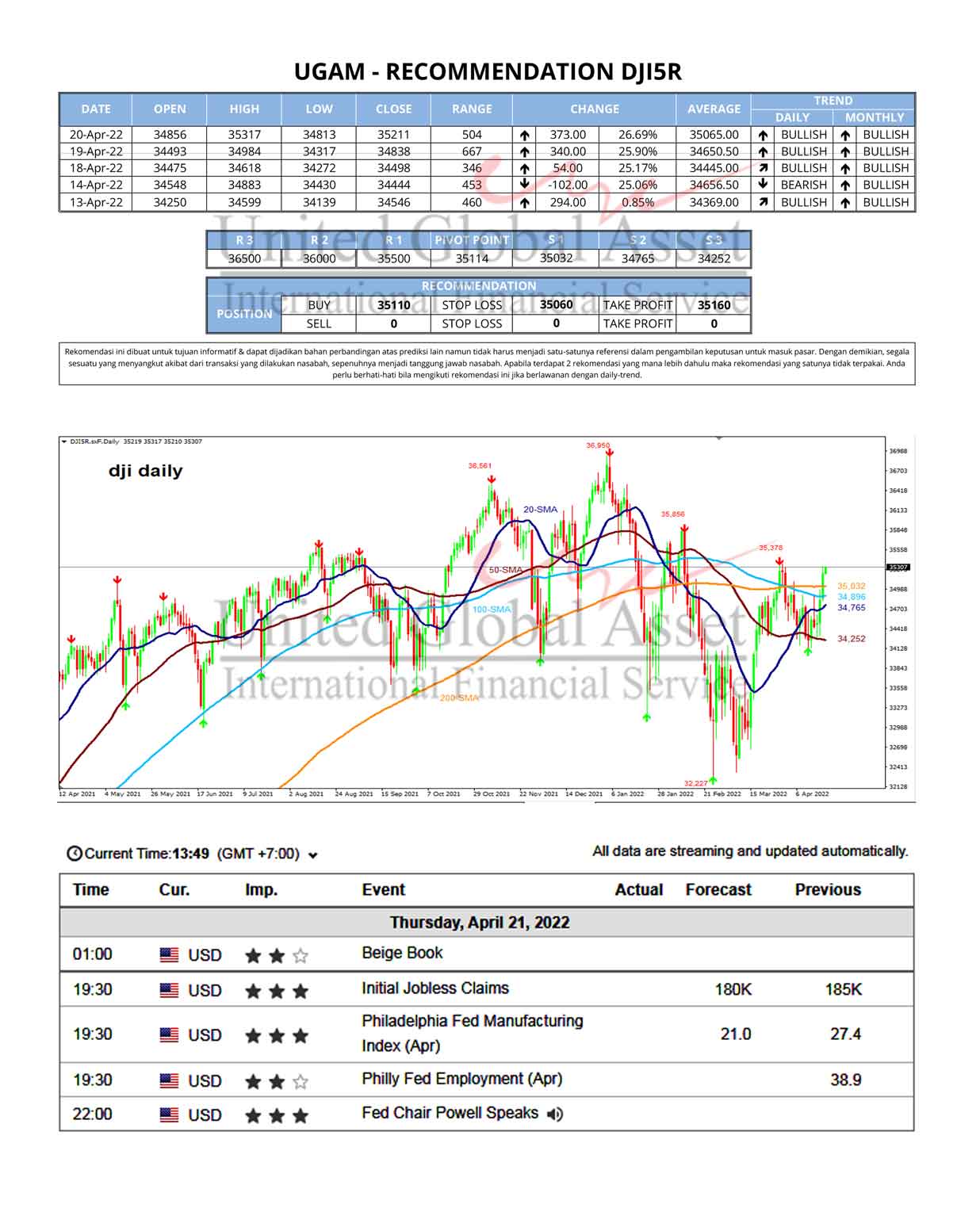

Fundamental News - DJI5R

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

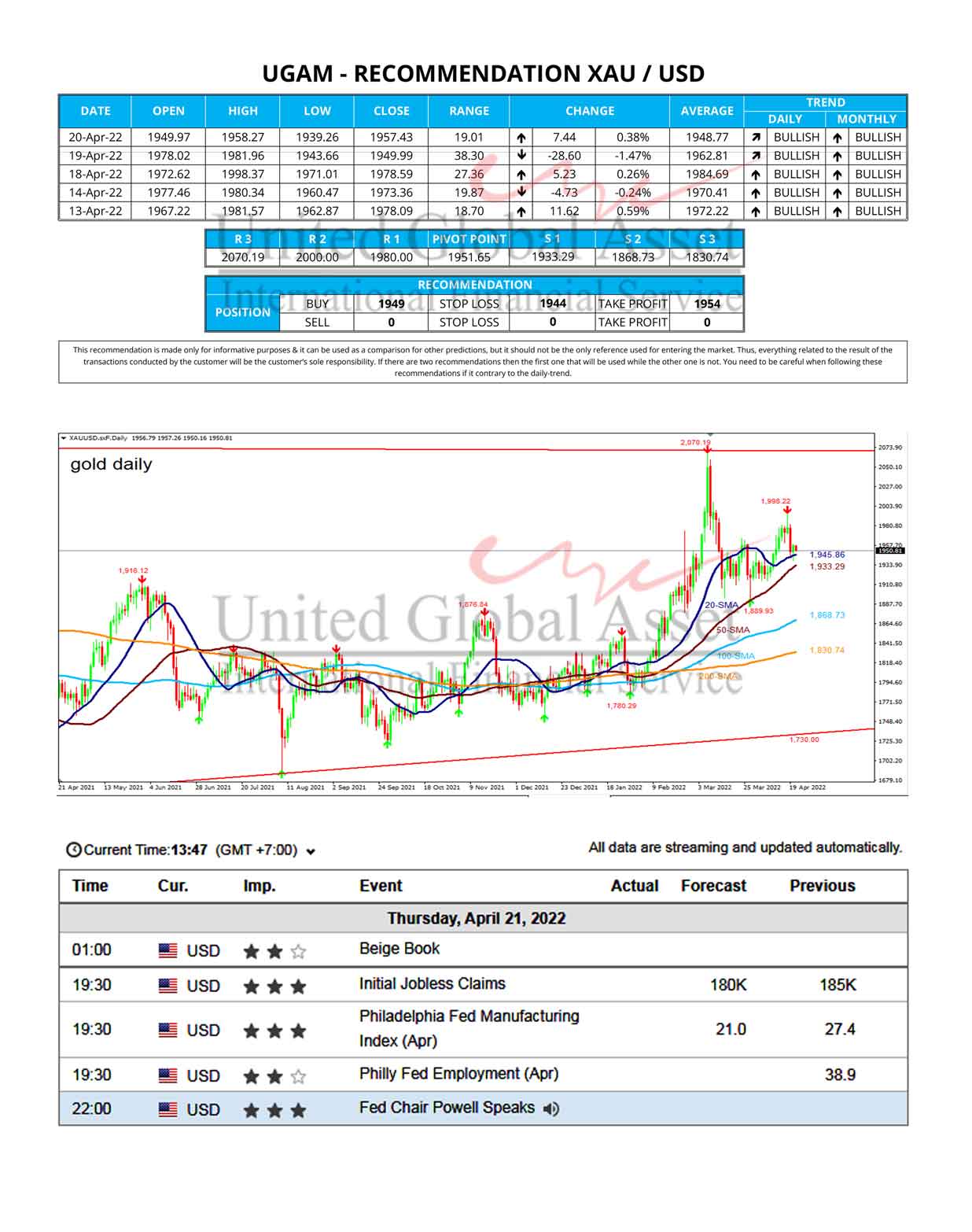

Fundamental News - XAUUSD

Gold Price is in a narrow consolidative range so far this Thursday having stalled its rebound just shy of the key $1960 level.Gold Price could see further downside risks in...