Earning Preview: Apple Inc.

Next week will be a big one for Big Tech, as the industry giants will step up to the earnings plate. None come bigger than Apple (AAPL), and on Tuesday July 27, the giant from Cupertino will deliver the June quarter’s (Q3FY21) financials.

While Apple and its Big Tech brethren are under scrutiny like never before, Monness analyst Brian White believes that Apple’s standing amongst consumers has only increased in the pandemic era.

“During this crisis, we believe Apple has enhanced its value proposition in the eyes of the world by introducing new innovations, supporting a more digital lifestyle, and attracting new consumers to Planet Apple,” the 5-star analyst said. “However, a changing political landscape and growing suspicion of Big Tech places Apple in a more vulnerable position than in past years.”

Google has roused the lawmakers’ ire recently and the Google Play Store is currently the subject of an antitrust lawsuit. White believes this “increases the chances of more scrutiny around Apple’s App Store.” Nevertheless, despite anticipating more probing from the lawmakers, the analyst continues to believe Apple remains “that ‘shining city upon a hill’ in the Big Tech world.”

Turning to the quarter’s display, the analyst expects Apple to “approach” White’s 3QFY21 revenue estimate of $80.33 billion, which will amount to a 35% year-over-year uptick and better the Street’s $72.94 billion estimate. On the bottom-line, White thinks Apple will “at least” meet his EPS forecast of $1.16, which is also higher than consensus, which calls for $1.00.

White’s estimates represent a sequential revenue drop of 10%, which is a touch “steeper” than the 4-year average 8% quarter-over-quarter decline of previous June quarters.

“Recall,” White wrapped up, “Apple did not issue a formal 3Q:FY21 outlook and we believe Street estimates are overly conservative.”

So, what does this all mean for investors? White sticks to a Buy rating and makes no changes to the $180 price target. Upside potential from current levels is 23%.

As with his FQ3 estimates, White’s assessment is more positive than the Street’s overall take; with the average price target clocking in at $159.42, the projection is for 12-month gains of 9%. The stock currently has a Moderate Buy consensus rating, based on 19 Buys, 5 Holds and 2 Sells.

Market Recomendation

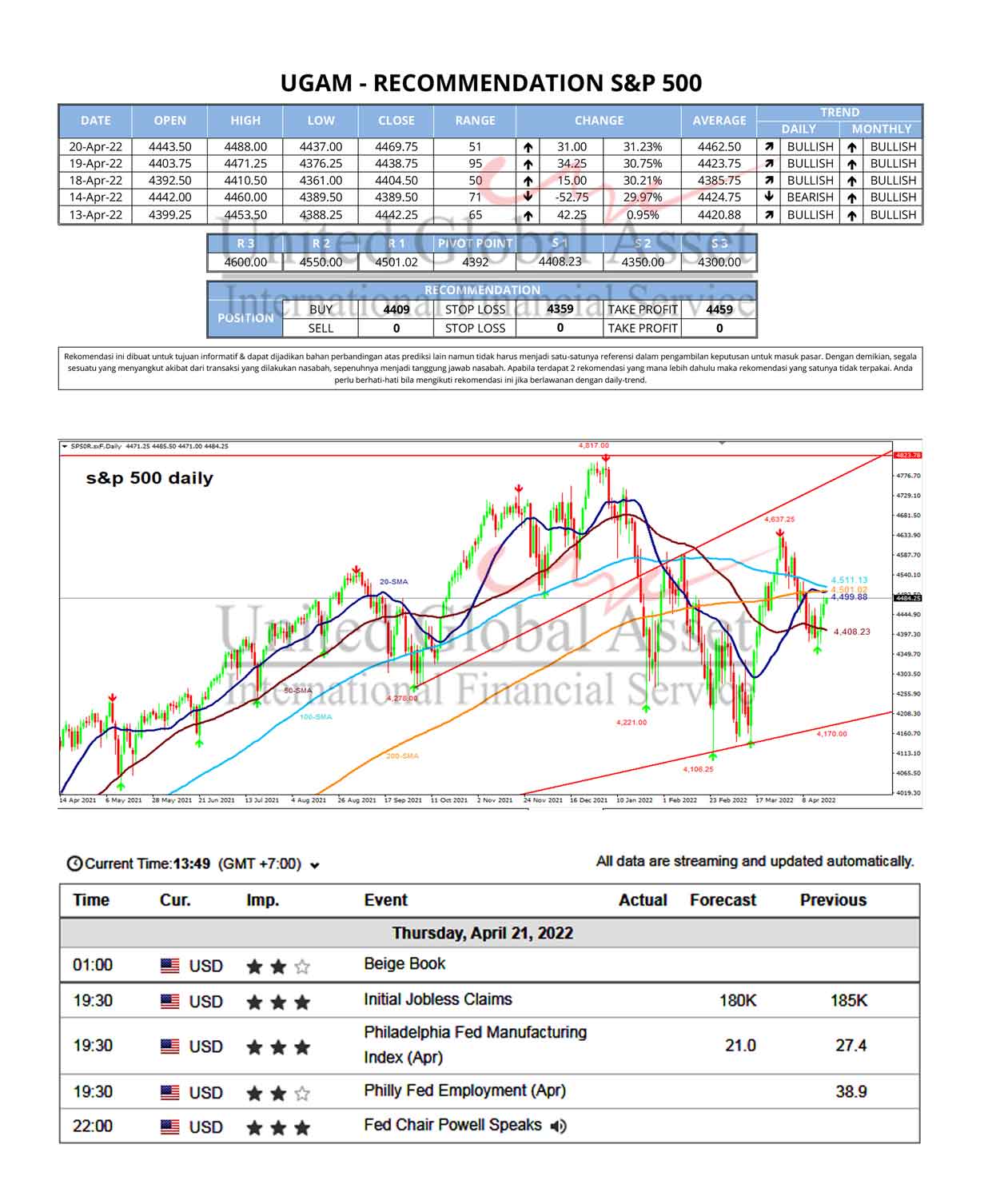

Fundamental News - S&P500

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

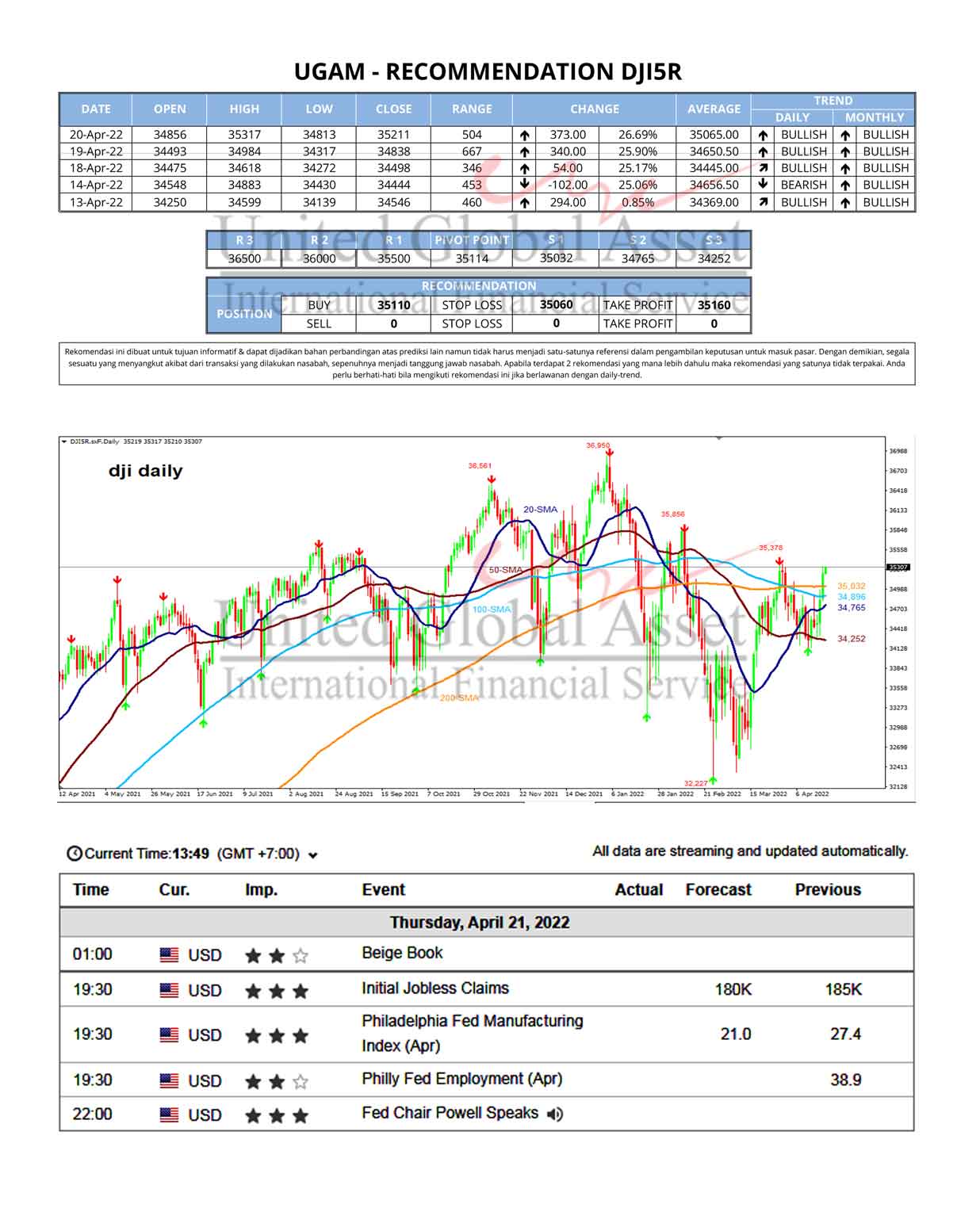

Fundamental News - DJI5R

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

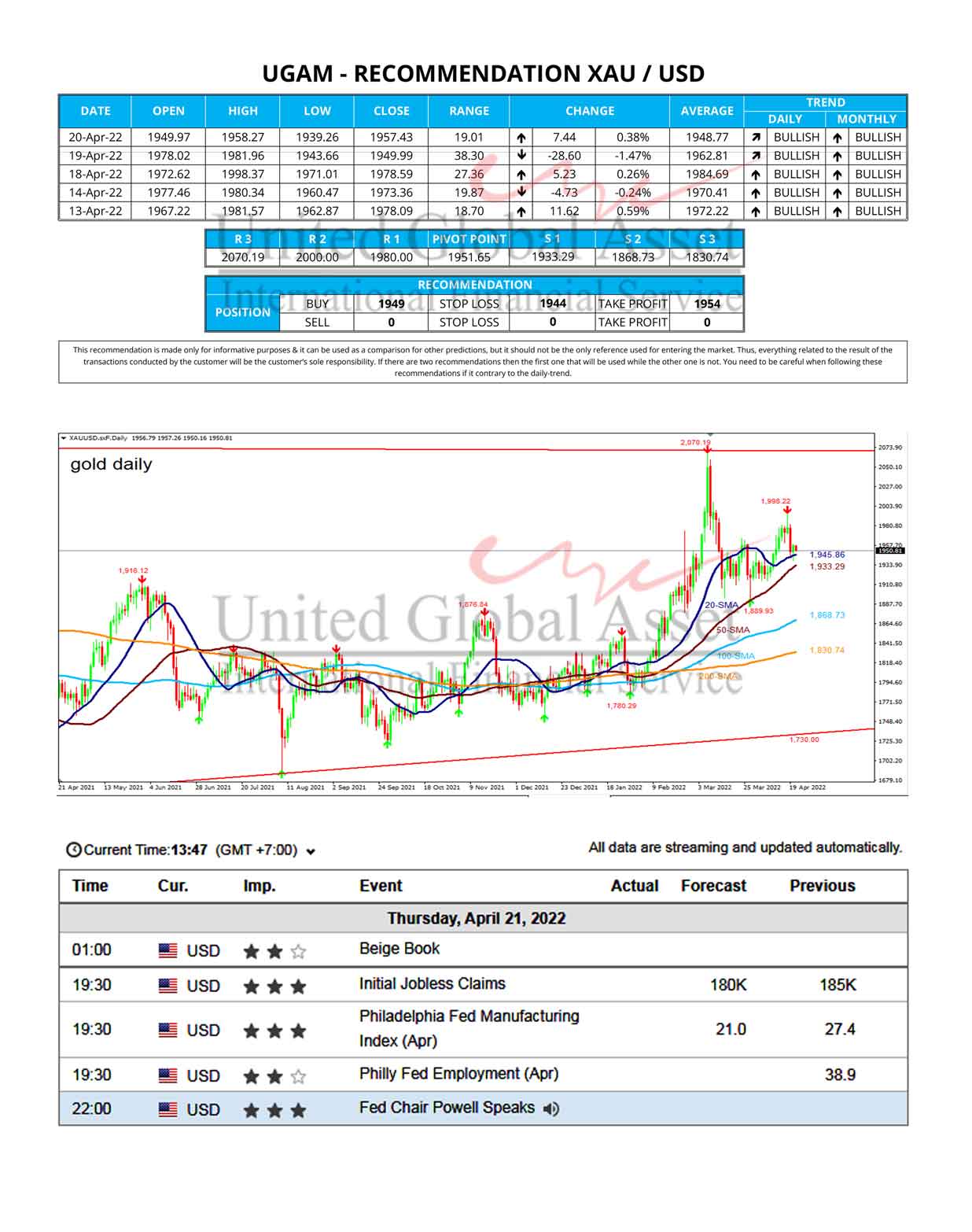

Fundamental News - XAUUSD

Gold Price is in a narrow consolidative range so far this Thursday having stalled its rebound just shy of the key $1960 level.Gold Price could see further downside risks in...