fundamental News - EUR/USD

EUR/USD dipped in wake of the release of the latest Fed minutes, with the accounts of the 14-15 policy meeting clearly exceeding what were already hawkish expectations. The pair, which was trading closer to 1.1340 prior to the release, is now trading around 1.1310 and eyeing a retest of the 1.1300 level, though still trades with gains of about 0.2% or over 20 pips on the day. For now, the 21-day moving average at 1.1307 is offering support. But if the hawkish tone of the latest Fed release can attract more dollar bulls out of the woodworks, the EUR/USD may be on course for a break below the big figure and a test of this week’s sub-1.1280 lows, which also coincide with last week’s pre-New Year’s lows.

Market Recomendation

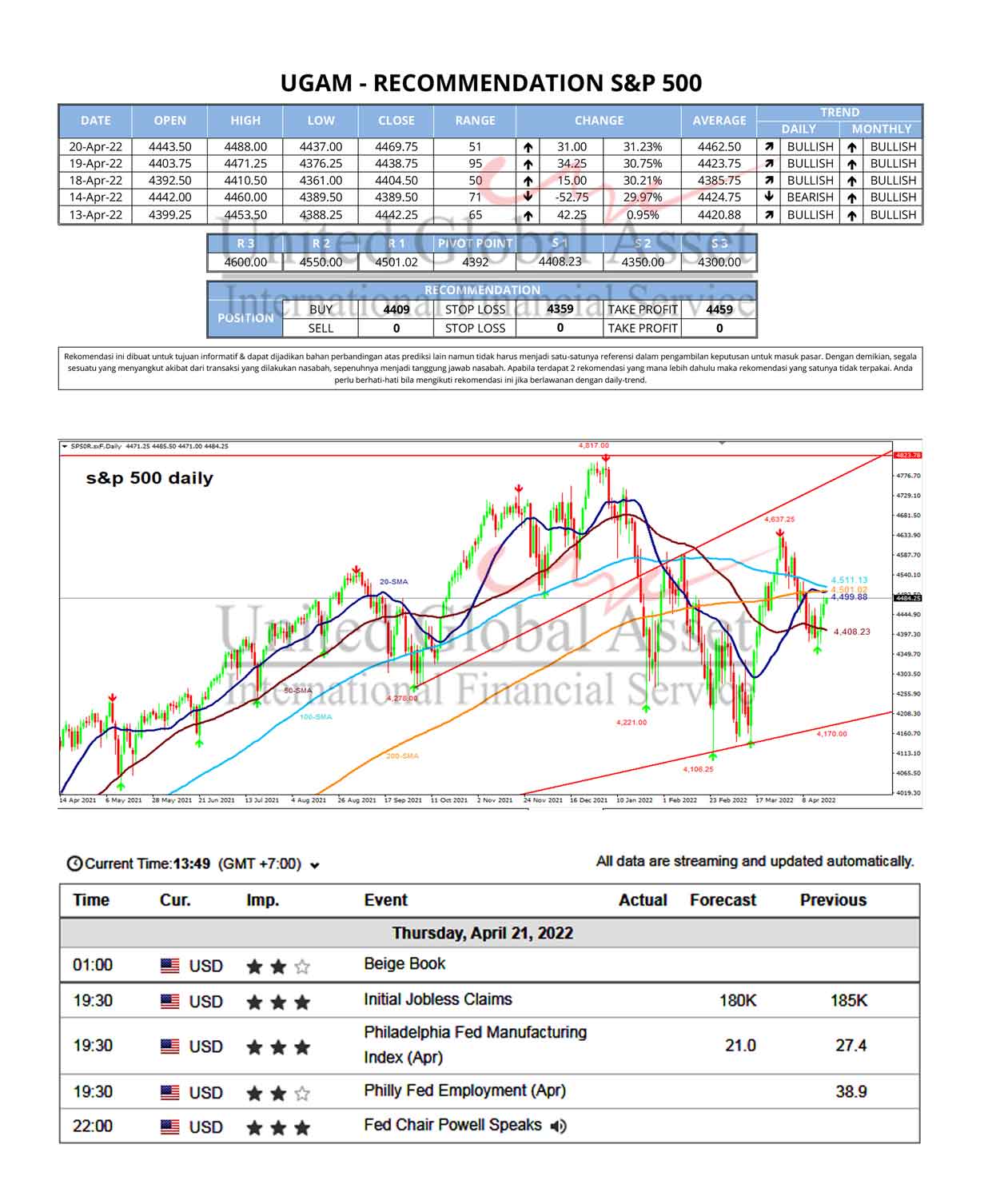

Fundamental News - S&P500

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

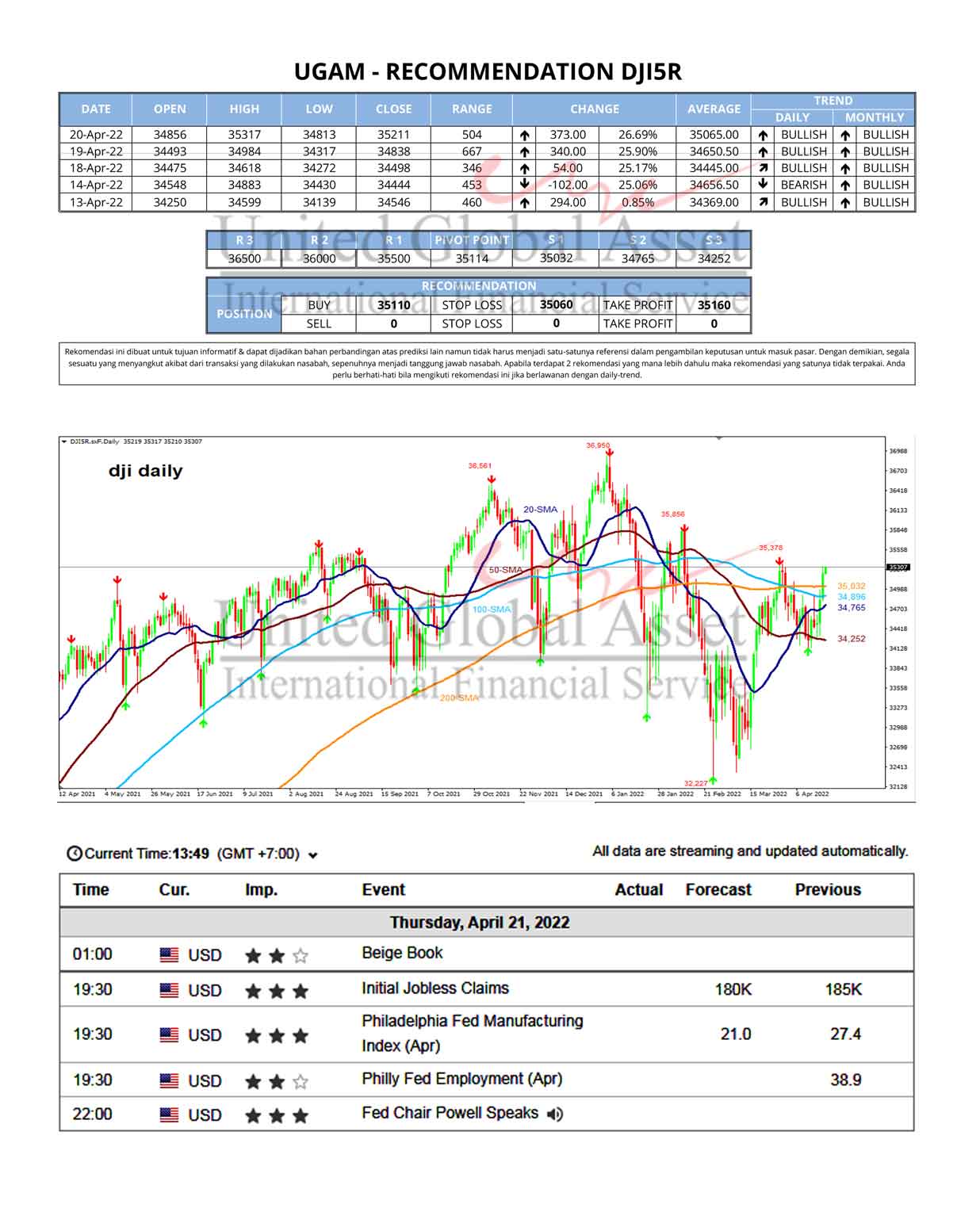

Fundamental News - DJI5R

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

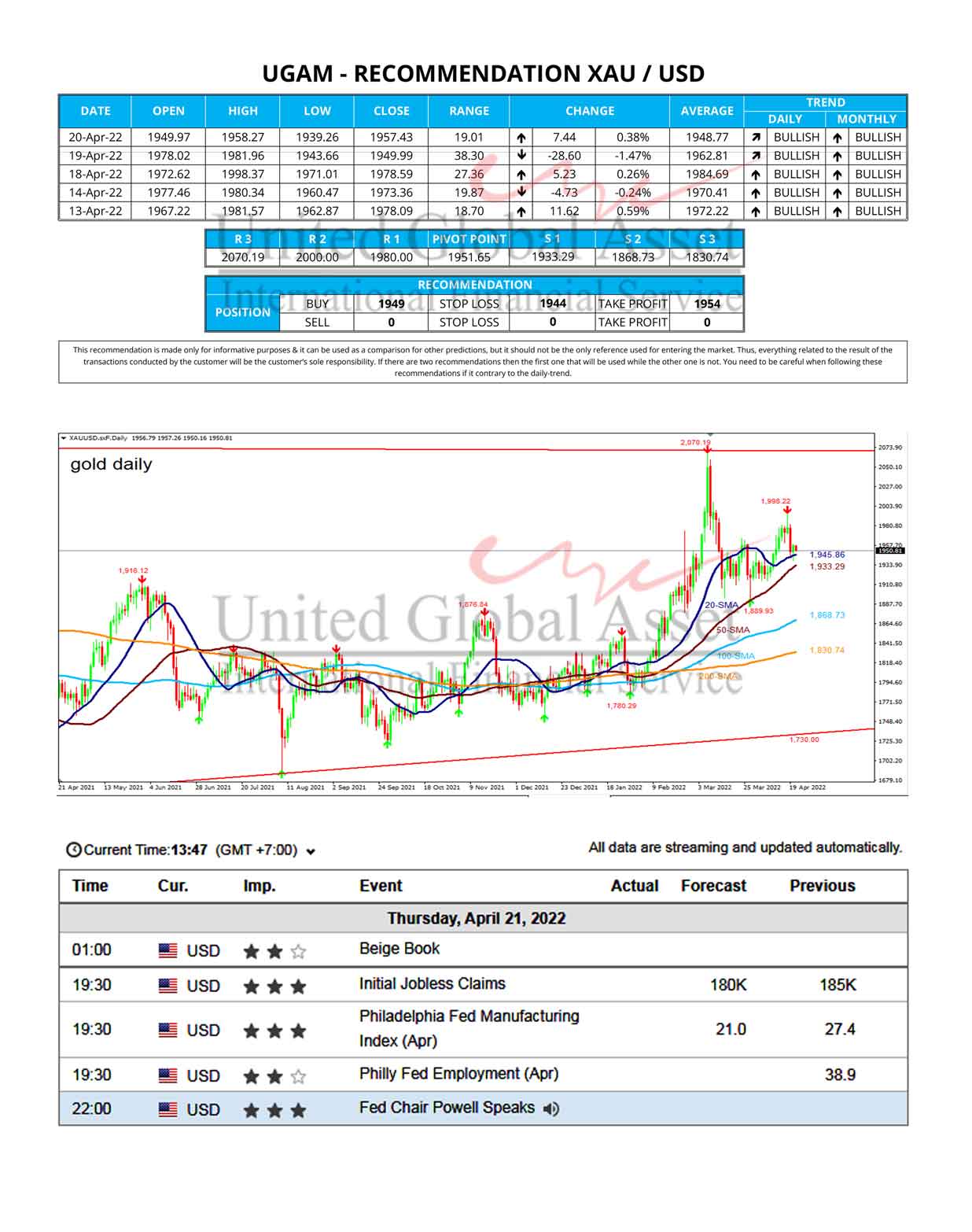

Fundamental News - XAUUSD

Gold Price is in a narrow consolidative range so far this Thursday having stalled its rebound just shy of the key $1960 level.Gold Price could see further downside risks in...