fundamental News - OIL

Oil was down on Tuesday morning in Asia, seeing a fourth consecutive day of losses over as the rising number of global COVID-19 cases lead to mounting fuel demand worries.

Brent oil futures fell 0.73% to $42.31 by 12:00 AM ET (4:00 AM GMT) and WTI futures was down 0.63% to $40.80. Both Brent and WTI futures remained above the $40 mark.

There are over 40 million COVID-19 cases globally as of Oct. 20, according to Johns Hopkins University data. A second wave of cases in Europe and the U.S. has seen governments re-introduce restrictive measures.

“Since April we have seen a miraculous recovery in oil demand, which is now at about 92% of pre-pandemic levels, but it’s too early to declare an end to the COVID-19 oil demand destruction era,” Rystad Energy oil markets analyst Louise Dickson told Reuters.Fuel demand concerns saw OPEC+ pledge to support the black liquid during Monday’s joint ministerial monitoring committee meeting. Despite the concerns, OPEC+ will press ahead with plans to pare production cuts to 5.7 million barrels per day (bpd) from January onwards, from the 7.7 million bpd cut in place through December. However, these plans to increase output from January could reportedly be reversed should the need arise.

“We don’t think oil markets are in a position to absorb the around 2% of global supply that OPEC+ are expected to restart from 1 January 2021,” Commonwealth Bank commodities analyst Vivek Dhar said in a note.

Rising output from Libya, which is operating outside the OPEC+ pact, was adding to oversupply concerns, the note added.

Libyan production is seeing a rapid increase, playing catch up after almost all the country’s output was shut down in January due to the outbreak of armed conflict. Sharara, the biggest field, is now reportedly at around 150,000 bpd, or half of its capacity, since it re-opened on Oct. 11.

Investors are now looking to crude oil supply data from the American Petroleum Institute, due later in the day.

Source: investing

Market Recomendation

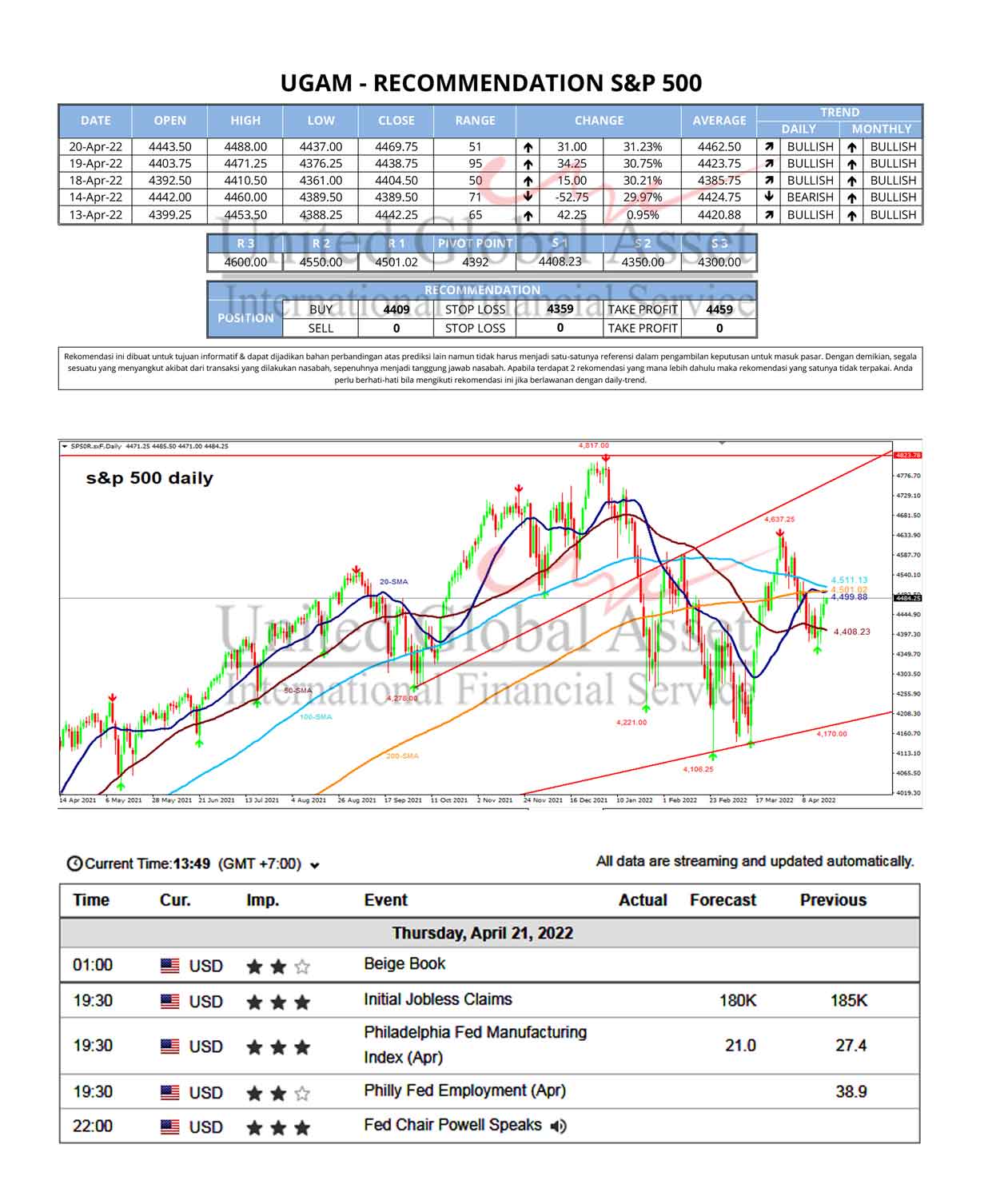

Fundamental News - S&P500

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

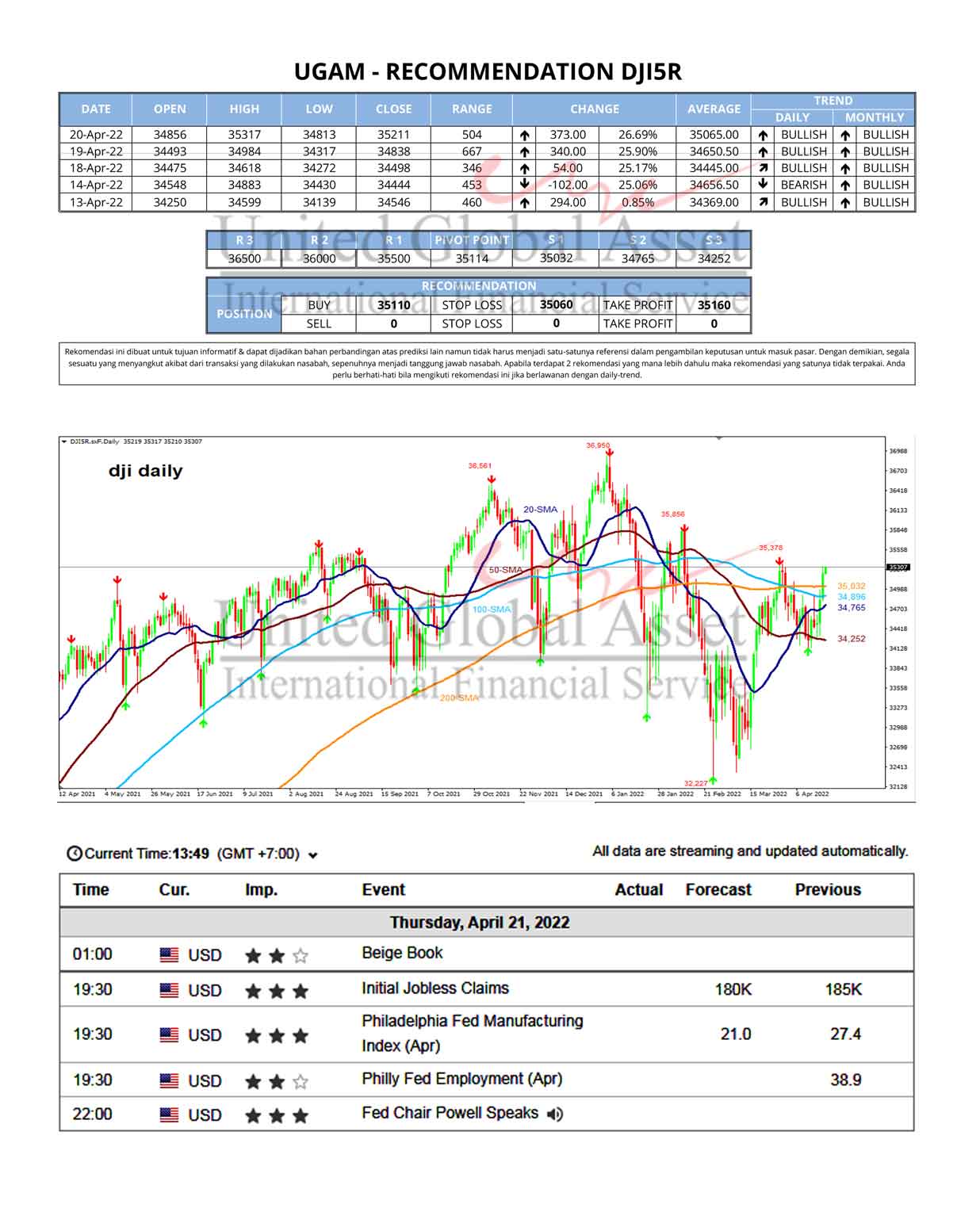

Fundamental News - DJI5R

US stock futures rose on Thursday after a mixed session on Wall Street as investors digested more quarterly reports against a backdrop of elevated inflation and further monetary tightening. Dow...

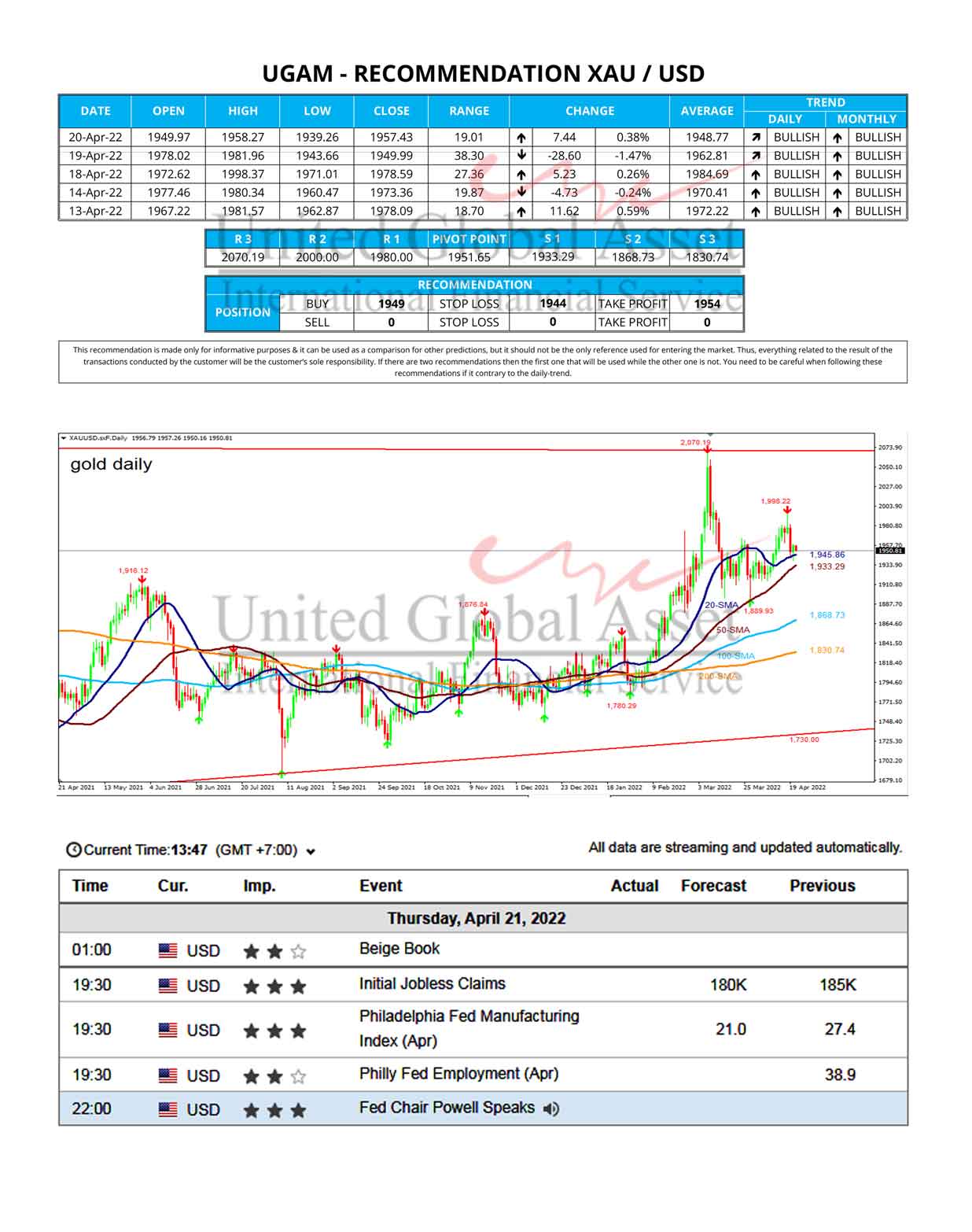

Fundamental News - XAUUSD

Gold Price is in a narrow consolidative range so far this Thursday having stalled its rebound just shy of the key $1960 level.Gold Price could see further downside risks in...